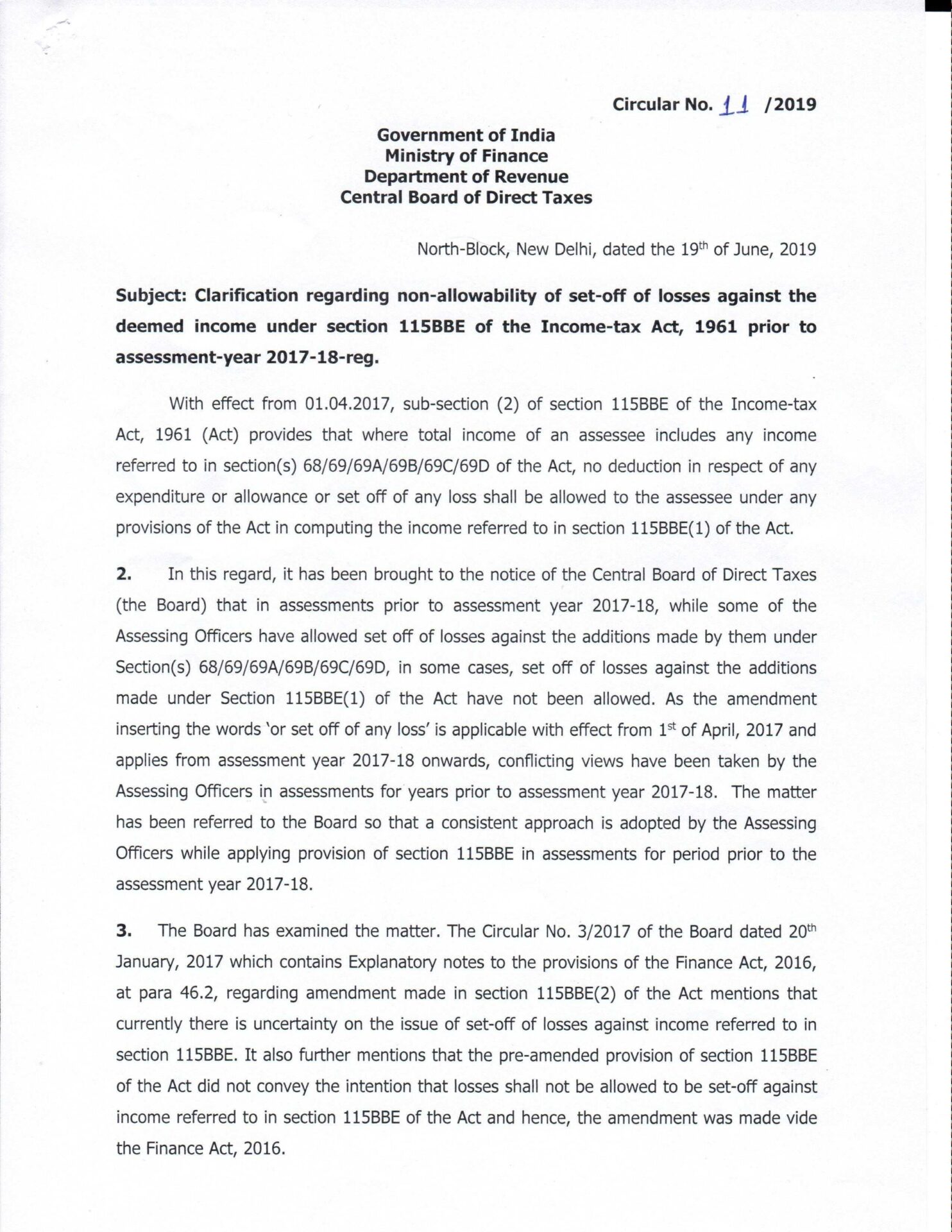

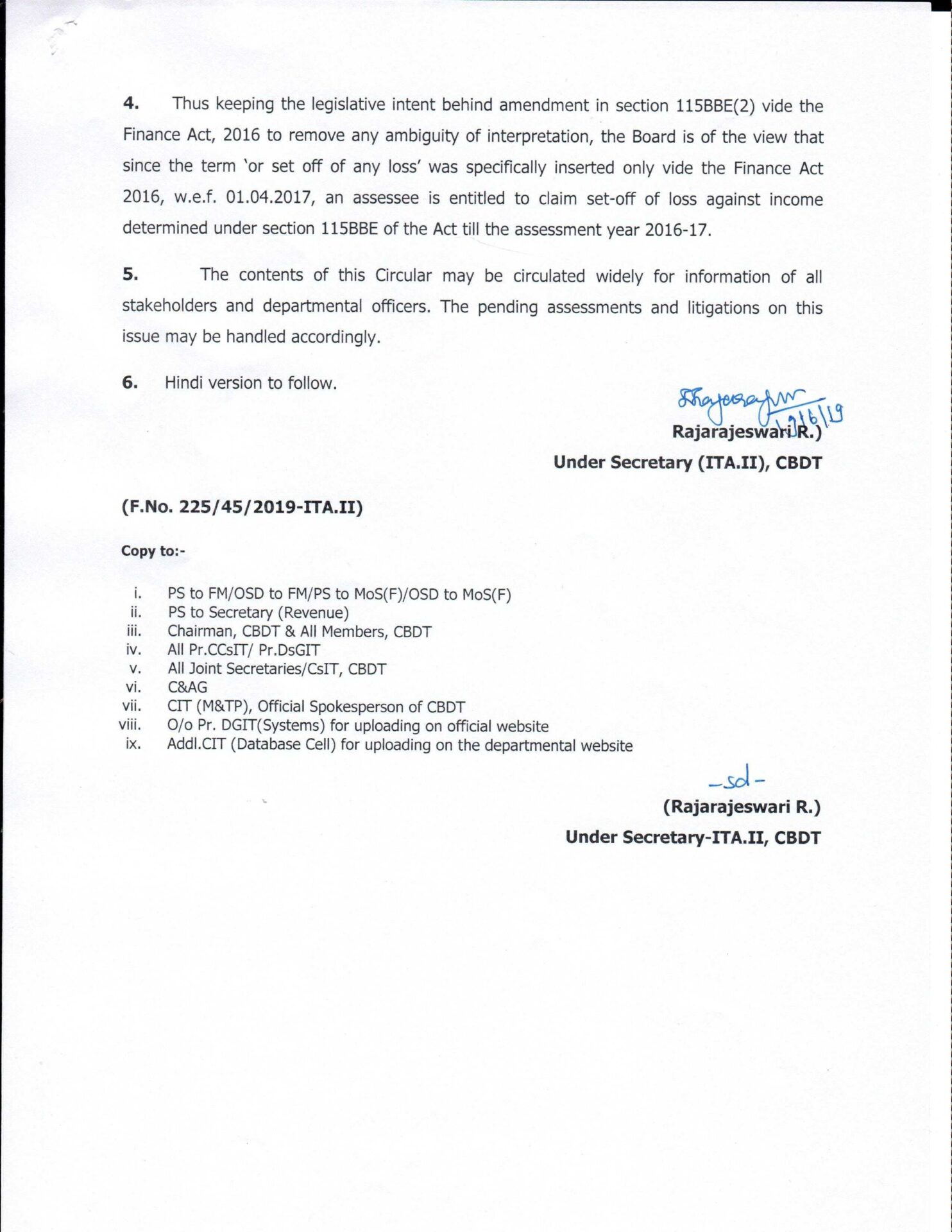

Income TaxLatestCircular No. 11/2019 Income tax – Clarification regarding non allowability of set off of losses against the deemed income under section 115 BBE by Team Taxcharcha19/06/201904083 Share0 non allowability of set off of losses under section 115 BBE